{kind=link}

Let’s forget for a moment that cryptocurrencies are basically banned in Pakistan.

Payment systems are as old as human society. Ancient Sumerian tablets were nothing more than ledgers; records of debit and credit. Since then, the payments industry has evolved exponentially – from it’s humble beginnings on clay tablets to the modern day blockchain.

With the advent of cryptocurrency, the potential for blockchain technology to radically alter the payments industry are being explored. While the practical use of cryptocurrencies such as Bitcoin for payments remains limited, the potential is limitless.

As we wait for cryptocurrencies to truly blossom as a disruptive technology in the payments industry, let us look at some facts that provide context and insight to where the industry is currently positioned.

Many of the findings below have been published in the Global Findex Database by the World Bank and 2017 World Payments Report.

1. International Payments are Still Not Easy

The most common method to making a payment is the same as it was a century ago. A customer walks into a bank during working hours, waits for his turn and withdraws or deposits cash or cheques. This whole process can be completed within a few minutes on working days.

Things become disproportionately complicated if one wants to carry out an international transaction, which can take a few working days using a financial network known as SWIFT.

Let us take an example, person A from China wants to send money to person B in the USA. Person A will go to a bank and ask his bank to make the transaction. This bank will verify if they have an account with Person B’s bank. If they do, the transaction will be carried out in a day or two. However, if they don’t, the banks will have to find an intermediary bank where both have an account. This process can be expensive and take several days. If the currency sent is different from the currency to be received the bank, there may be further delays in search for a reasonable exchange rate.

2. Online Payments were not Always This Popular

Those disheartened by critics of cryptocurrency adoption can seek inspiration from the early days of online banking. During the early 1980s, online banking was a novel idea which couldn’t gain much traction due to procedural complexities and a general lack of trust on behalf of the customers. In the 1990s, as people became more comfortable with the high-speed internet, online banking gradually began to increase in popularity. The smartphone revolution has served as multiplier; today, some customers rarely visit their banks after their accounts are opened.

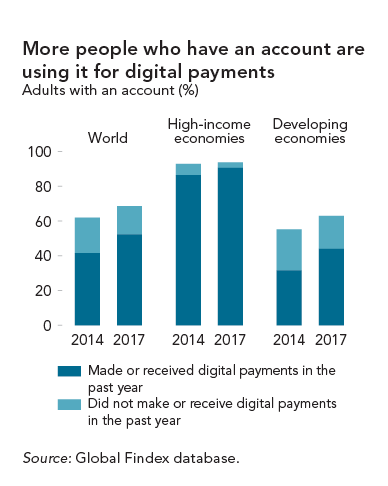

3. Bank Accounts Are The Safest Passage to Digital Payments

Online banking is the preferred mode of banking in developed countries these days. Developing countries are also gradually adopting the new advancements. From 62 percent of people in developing countries who have bank accounts, almost two-third had made or received digital payments in the last year. This trend can be largely attributed to smartphones.

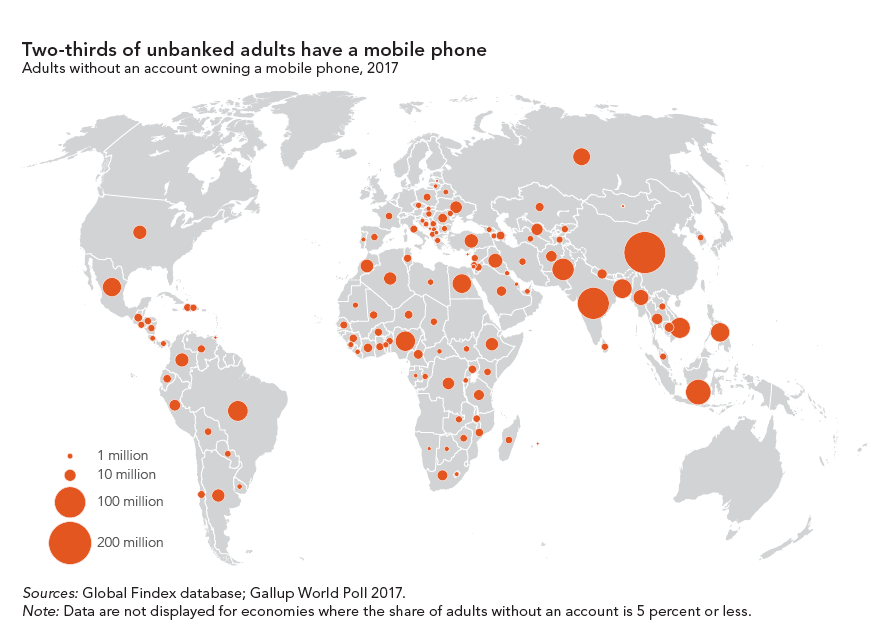

4. 1.8 Billions Adults Still Don’t Have Bank Accounts

With all the talks about digital payments, it needs to be highlighted that a whopping 1.8 billion bank account. This means that their likely mode of payment remains through cash. This would be a truism if it wasn’t for a little trend cooking up in Africa.

5. Mobile Money Accounts are an Epidemic in Central Africa

Remember what we wrote about mobile phones? For anyone lucky enough to go to the faraway regions of Africa or Southeast Asia, it would not be a surprise to know that mobile phones are much more common than bank accounts.

The figure below shows that amongst the 1.7 billion people who do not have a bank account, more than two-thirds have a mobile phone.

They say that necessity is the mother of invention. Mobile money accounts have spread rapidly in the western and eastern ends of the continent; regions which generally have less bank account holders. Mobile accounts are a simplified alternative to bank accounts, therefore their lack of popularity in countries (Egypt, Algeria) which have more developed banking networks.

6. Modern Payment systems are still quite Vulnerable

The inclusion of technology into the payment industries has introduced it’s share of security threats and vulnerabilities. When using a website, mobile phone and other digital mediums for payments, a user is quite susceptible to hacking and phishing attempts. ATMs too are easily rigged by hackers, results in millions of dollars of theft each year.

According to PwC’s 2018 Global Economic Crime and Fraud Survey:

- 49% organizations have been victim of fraud or hacks; the value spiked from 36% just half a decade ago.

- 52% frauds were carried out by the help of an insider.

7. 40% of households depend on Credit Cards to pay basic living expenses

World Bank’s Global Findex Report of 2017 states that ‘studies have shown that mobile money services— which allow users to store and transfer funds through a mobile phone— can help improve people’s income-earning potential and thus reduce poverty. A study in Kenya found that access to mobile money services delivered big benefits, especially for women. It enabled women-headed households to increase their savings by more than a fifth; allowed 185,000 women to leave farming and develop business or retail activities; and helped reduce extreme poverty among women-headed households by 22 percent.

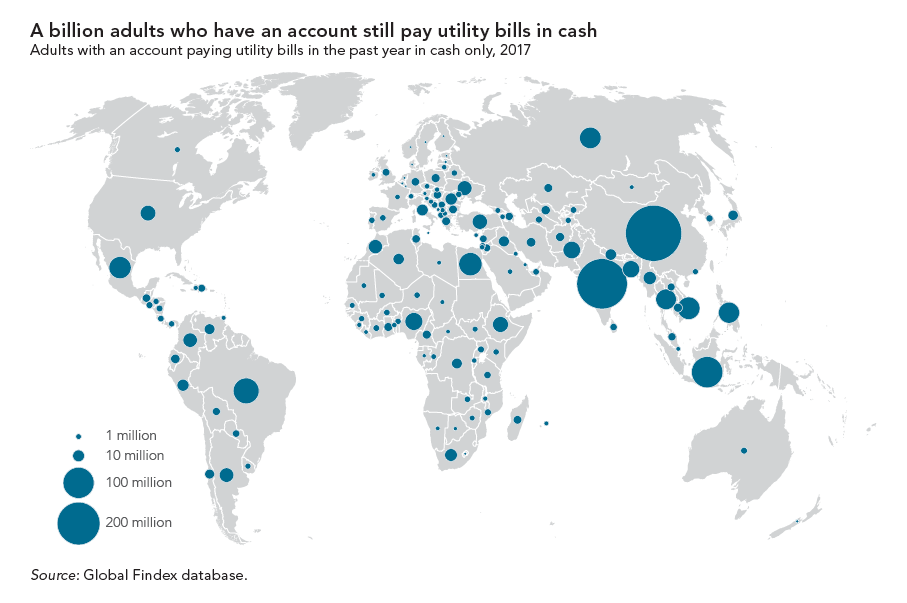

8. A Billion Account Holders Still Pay Utilities in Cash

They say old habits die hard: the GFD analysis has highlighted that over one billion adults with bank accounts still pay utility bills in cash. This may lead to two mutually compatible assumptions:

- Utility companies still have not adopted convenient procedures for online / banking payments with efficient monitoring

- Social habits, such as making certain payments in cash, may take a long time to change and may outlive their rational utility

9. 72 percent of US online shoppers have a PayPal Account

In an article on Securetrading.com, it is highlighted that a whopping 39 percent of online payments are made through PayPal. This is second only two credit card payments (through Visa & Mastercard) and exceeds payments by debit card (28 percent).

Paypal enables a secure means of sending and receiving payments for all types of buyers and sellers, thus ensuring it’s popularity and farspread adoption by online merchants.

10. Credit Card Debt has exceeded $1 trillion dollars

You have read that right: Credit Card debt in the US has exceeded $1 trillion dollars. To put that into perspective, that’s right about the same as Mexico’s GDP in 2016.

As highlighted in the last point, Americans love using credit cards for all array of goods and services. This is complimented by the fact that credit card fees and rules are usually more lenient in the US as compared to most other countries.

Blockchain cryptocurrency developers are fast on the heels of major banks to provide a technology that is convenient, faster and secure than prevalent modes of payment – both digital and traditional. Proponents of cryptocurrencies claim that the technology is:

- Safer: The encryption of blockchain does not let an outsider to commit fraud or alter transactions easily.

- Cheaper: In average, it will cost around $1 (instead of the $5 current average) for a single blockchain transaction; this will likely go down further in the future.

- Faster: While it varies from blockchain to blockchain, a cryptocurrency average for the processing of a single block is 10 minutes, which is much faster than the traditional way of sending money through a bank to another country.

Technology has significantly altered the payments industry. When more people have access to carry out financial transactions easily, their chances of income and standard of living improves. This also has numerous benefits and opportunities for traders and merchants. With the advent of blockchain technology, it is not a question of ‘if’, but ‘when’ it will be recognised as a truly disruptive technology in the payments industry.